Disability

This provides a replacement for a person's most important piece of paper, their pay cheque. If you are independently wealthy, this won't be a concern. If, however, you cannot work due to illness or injury, and there is no money coming in, financial disaster will be the result. Insurance is the life vest you want to be able to inflate if catastrophe hits. Ambulances pass by regularly, sirens wailing, and you hope that you never have to go for a ride as a customer. If you did, and six months later were still unable to collect a pay cheque, where would the money come from for mortgage, rent, and living?

If you are fortunate enough to have insurance as part of your group plan, find out what the amount is. Usually it's about two thirds of your salary. If the cost of that portion of the group plan is paid by you, the money will come tax-free. If the employer pays, it will be taxable. If you're self-employed or there is no group plan where you work, individual disability insurance is available. The cost and type of coverage you may get will depend on a number of variables. Disability insurance is more complex than life insurance. There are a lot of ways to become disabled, you only die once. What a disability insurer has to consider is:

- What is the risk of the occupation the applicant works in?

- What is the claims experience of that type of work?

- What is your age?

- How long do you want the coverage to pay?

- How soon after the event do they have to start sending money?

- What guarantees are put into the policy contract regarding definitions and ability to adjust the price later due to adverse claims experience?

- The definition of disability is the most important section of the contact. It defines how you do or do not get paid. Of all the insurance plans written, the most law suits spin around this product.

Here are four definitions of total disability offered by various insurers:

- You are totally disabled if you are unable to perform the material and substantial duties of your own occupation to age 65.

- You are totally disabled if you are unable to perform the material and substantial duties of your own occupation to age 65, AND you are not working in another occupation.

- If you become totally disabled as a result of accident or sickness while insured, you will receive a monthly benefit. During the first 24 consecutive months, total disability means your continuous inability to perform substantially the essential duties of your regular occupation. Thereafter, total disability means your inability to engage in any occupation for which you are qualified or may become qualified through training, education, or experience.

- You are totally disabled if you are unable to perform the duties of any occupation to which you could be expected to perform with due regard to your training, education, or experience.

There is a big difference in risk and requirement to pay between “own occupation” and “any occupation”. Most individual policies have an “own occupation” definition. Group plans are usually 2 year “own occupation” and then from the 25 th month on, “any occupation”. In the economy plan, it is “any occupation” from day one.

Actually, many claims are not “total disability”. Many people are partially disabled. They work, but a condition prevents them from being 100% efficient and they suffer a reduced income as a result. Does your policy have a clause for this possibility? If your plan does not have a provision for a partial/residual claim, a return to work (even if just a day a week) could disqualify your claim.

The leading cause of LTD (Long Term Disability) claims is cancer . The other four are: pregnancy complications, back problems, cardiovascular conditions , and depression . This list comes from Unum/Provident's database, the largest database of disability information in the U.S. Half of the LTD claims come from those 5 conditions. The most common age for an LTD claim is 56.

To make an application for a LTD plan, you will have to provide proof of income. If you have a history of a sore back, tennis elbow, or other seemingly minor ailment, be prepared for an exclusion. Also, be patient. Underwriting this type of plan can take 2 to 3 months form start to finish, depending on how quickly various doctors' reports can be obtained.

The onus will be on you to provide proof of income. Have your tax returns and corporate financial statements available. A copy of these will have to be included with your application.

The Best Financial Decision I Ever Made.

Initially I thought the cost was high: $250 a month, but I viewed it as an investment in myself, my business, and my family. Never did I think I would have to use it. I would notice the cost on the annual financial statements. By 1996, my premium had increased as had my coverage.

Life sometimes works in unforeseen ways. I noticed my ability to move and walk any distance causing distress. The diagnosis: Arterial Occlusive Disease, or hardening of the arteries in my legs. I was forced to wind up the business and have tried to find new pursuits which require little physical exertion.

|

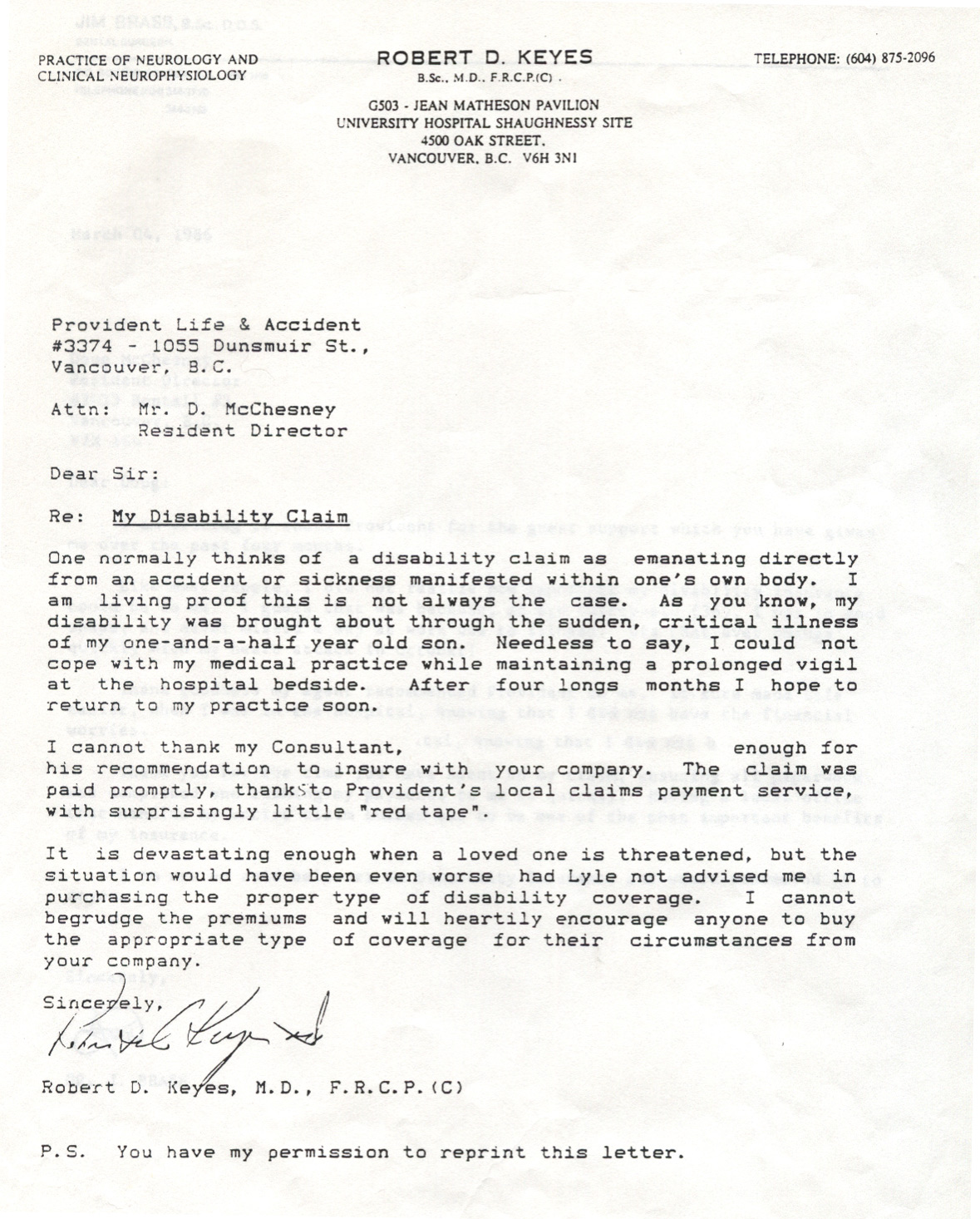

LEFT: This man learned the hard way what ‘any occupation definition' means at claim time. RIGHT: This letter is from a doctor who had a true ‘own occupation' policy. The stress of critical illness in his family was enough to qualify a claim. |

|

|

LEFT: This claimant had a 2-year own occupation group coverage. It is now suggested that he consider any occupation employment such as an ‘inventory clerk'. RIGHT: The first cheque to a client after a head injury. It would take 8 months to get the balance. Client could not fill in the forms due to confusion caused by T.B.I (Traumatic Brain Injury). Only after I discovered the extent of the problem with paper work could I finally get the claim settled. |

|

|

“The frequency or probability of loss is irrelevant. It must be measured with the magnitude of the outcome”

|

Read Real Stories

|

What People are Saying:

"Best financial decision I ever made!”

- M.P.

“You can only trust a company with knowledge, and InsuranceForMe is the best!”

- John Smith |