Self Employment

|

As the traditional corporate jobs downsize, vanish or change, Canadians are starting their own business and giving up the security (if there ever was such a thing) of the company paycheque. Of course what one also gives up is the benefit plan that provided extended health, dental, life and disability insurance. Can you replace them? Yes and no... The products and plans are available to the self-employed, but you probably cannot afford them all. Here's what you can look at if you value the idea of putting an umbrella of protection over your head. |

|

The unknown risk to any entrepreneur is disability. You can protect yourself with an individual disability plan. A couple of obstacles to overcome are: Can you show an income that will convince an insurance underwriter to issue you a policy? Can you afford the cost? The "cheap" disability insurance you had once under a group plan is no longer there and it may now cost $100-$200 a month for a proper policy, depending on age, smoking status, how soon, how long and how much. To answer all your questions might require a face-to-face discussion. There are plans that provide 'accident only' benefits or a more restrictive 'any occupation' type of definition that are more affordable. |

|

Life insurance can be purchased by your company or yourself. The banks feel "comfort" when you can show that you are prudently covering some risks. They will now even try to sell you their own product as they try to expand their web of services and fees deeply into your account. Some things to remember: since anytime you buy insurance it might be the last time you qualify medically. Consider the long term quality of your policy. What is the renewal cost in the future? Is there a waiver of premium provision attached? What is that definition? What are you conversion options?

Companies can cut the cost of a

term policy by pricing the renewal so that after the initial term period

you are encouraged to go and requalify medically. That's fine unless in

the meantime you develop something like high blood pressure, an ulcer

or heart problems. So all those 'low cost' plans now don't look like

such a good deal. I consider all the what if's and only recommend plans

that give you a value now and in the future. The five or ten bucks a

month you 'saved' might be the most expensive and disappointing decision

you'll regret later. Group, Association, and $1.49 Term Insurance from

the Automobile Association just don't provide the guarantees. If your

business is successful and creates the income and wealth you hope for,

you are going to want to use the tax planning and wealth transfer

opportunities life insurance offers. So the ability to change your

insurance plans without providing good health and going through the

application process can be a real benefit. "Do it right the first time

and you won't have to do it over later."

|

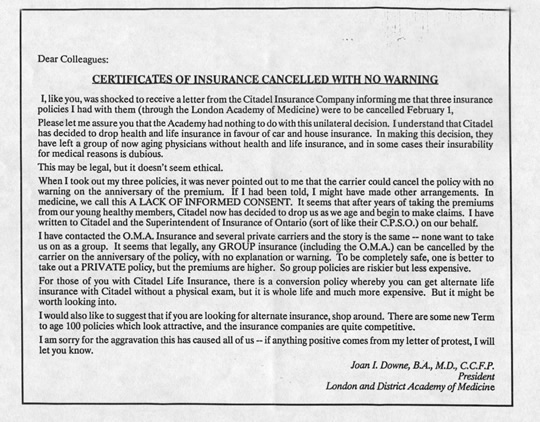

LEFT: This note informs a group of doctors that their insurance plan has been withdrawn. Be aware that group insurance can be cancelled or changed without your consent as a plan member. |

|

“The frequency or probability of loss is irrelevant. It must be measured with the magnitude of the outcome”

|

Read Real Stories

|

What People are Saying:

"Best financial decision I ever made!”

- M.P.

“You can only trust a company with knowledge, and InsuranceForMe is the best!”

- John Smith |